June 20, 2025

Despite a wave of fresh data and global developments, cotton prices held steady, stuck in a narrow range as the market digested weaker retail sales, steady Fed policy, and rising geopolitical tensions. With headline risk still elevated and uncertainty lingering, could the coming weeks bring more clarity, or just more noise? Get QuickTake’s read on the week’s events in five minutes.

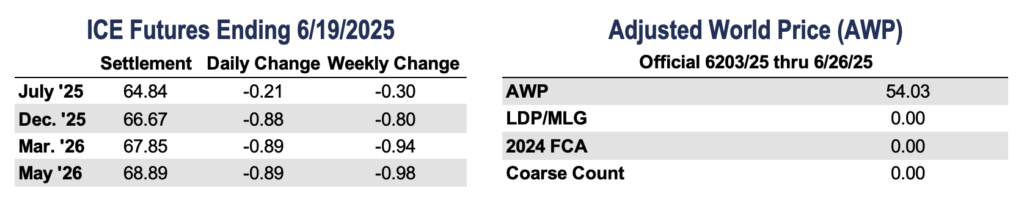

Cotton prices moved lower in the holiday-shortened trade week.

- July futures decreased a modest 30 points during the week, settling at 64.84 cents per pound.

- With the July contract all but gone, focus has shifted to the December contract. December futures closed at 66.67, down 80 points on the week.

- The market remained mostly rangebound with a short trading week and First Notice Day for the July contract quickly approaching on June 24. The imbalance between grower on-call purchases and on-call sales has prompted additional merchant selling ahead of First Notice Day. Similar to recent weeks, geopolitical tensions and lingering trade uncertainty added to the cautious tone.

- Trading volume was moderate this week, and open interest fell by 14,923 to 217,909. Certificated stocks climbed a marginal 120 bales to 62,332 bales.

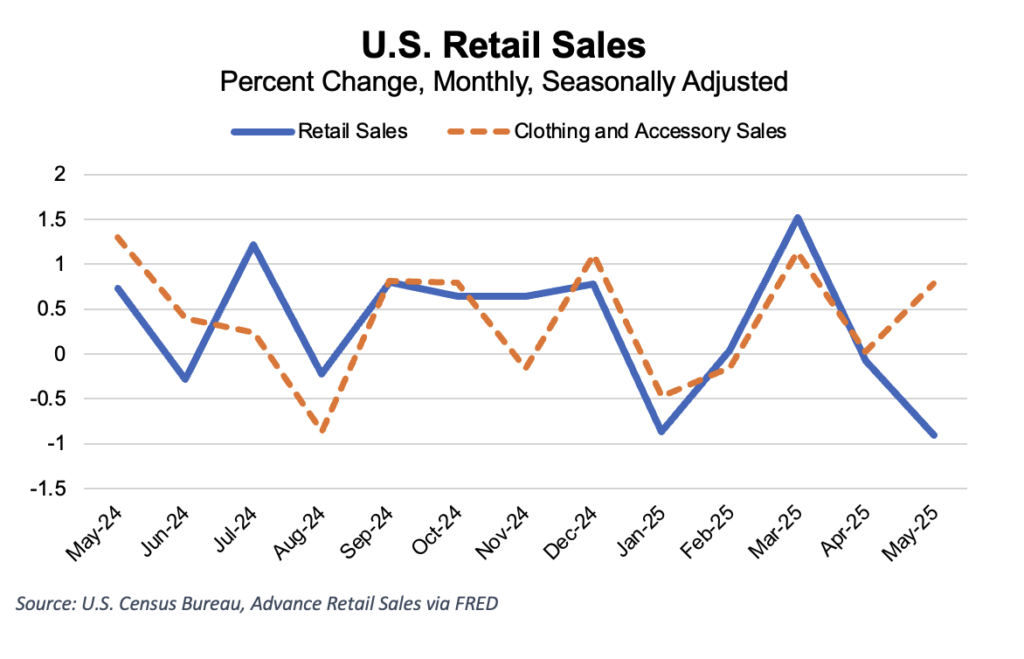

Markets held steady this week as traders navigated ongoing geopolitical tensions, softer economic data, and growing debate in Washington over fiscal policy.

- Retail sales dropped 0.9% in May, a steeper decline than expected and a potential sign of softening consumer demand. Annual growth also slowed to 3.3%, down from the previous month. While the headline numbers were weak, categories like clothing and home furnishings posted modest monthly gains. Still, broader declines in discretionary spending point to pressure from higher prices and interest rates. But with clothing sales holding up, it’s a bit of a double-edged sword, with signs of overall consumer caution, yet resilience in areas that are tied to fibers, like cotton.

- The Fed held rates steady in a range of 4.25-4.5% for the fourth straight meeting and continues to pencil in two rate cuts in 2025. While inflation has cooled somewhat, policymakers remain cautious, opting to wait and see how upcoming economic data unfolds. Higher interest rates can dampen commodity demand and global trade, so the Fed’s tone remains a key market signal.

- Oil markets rose this week as geopolitical tensions escalated in Eastern Europe and the Middle East. Renewed attacks in Ukraine, Red Sea instability, and increasing friction between Israel and Iran, alongside ongoing OPEC+ production cuts, kept prices firm.

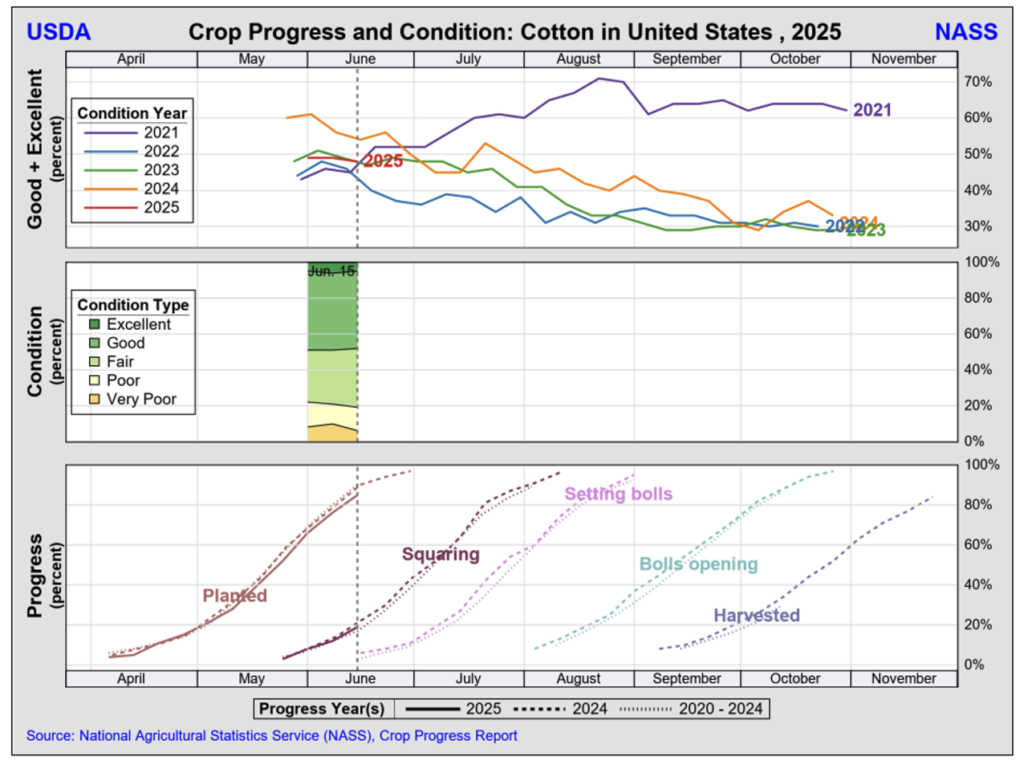

Planting across the Cotton Belt reached 85%, a few points behind the average. In the Southwest, Kansas is 92% complete, Texas is at 83%, and Oklahoma remains behind at 65%.

- Squaring has reached 22% in Texas and 2% in Kansas, while progress in Oklahoma remains minimal. Boll setting has begun in Texas, with 5% reported.

- Conditions are mixed. In Texas, 35% of the crop is rated good to excellent. Oklahoma and Kansas are in better shape, with 39% and 76% rated good or excellent, respectively. Wet weather earlier in the season slowed planting, and while conditions have improved, emergence and stand quality remain uneven in some areas. The rest of the Cotton Belt has also faced below-average conditions due to cooler temperatures and excessive rainfall.

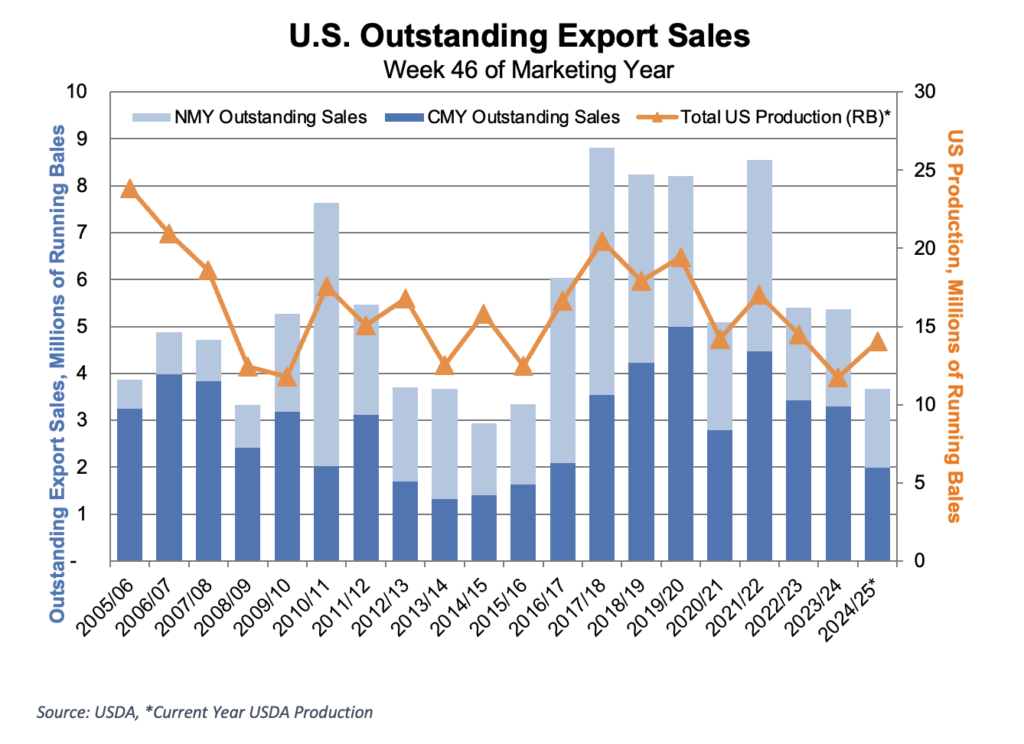

Current crop year sales remain sluggish, but new crop demand was encouraging for the week ending June 12.

- For the 2024/25 marketing year, U.S. merchants booked a net 83,200 Upland bales – slightly improved from the prior week but still trailing the 4-week average. New crop sales were encouraging to the market at 274,900 bales, with Vietnam, El Salvador, and Honduras leading the way. Shipments totaled 204,700 bales, lower than last week and the monthly pace, though still ahead of what’s needed to meet USDA projections.

- Pima activity was weak, with net reductions of 1,900 bales for the current crop year, marking the lowest weekly total so far this season. New crop sales totaled 6,500 bales, while shipments fell to just 3,000 bales.

The Week Ahead

- Next week marks a return to a fuller trading schedule, with a packed slate of economic and cotton-specific updates. Key reports include Consumer Confidence, GDP, and Personal Income, which will help shape market sentiment.

- For cotton, traders will be watching the weekly Crop Progress and Export Sales reports, along with the highly anticipated June 30 Acreage Report from USDA. Many in the industry are eager to see if adverse weather across the Cotton Belt led to a planted acreage figure below the current estimate of 9.867 million acres.

The Seam

As of Thursday afternoon, grower offers totaled 41,935 bales. There were 2,244 bales that traded on the G2B platform that received an average price of 63.39 cents per pound. The average loan for these bales was 53.07, bringing the average premium received to 10.32 cents per pound.